Silver is my favorite PM. There is less of it above ground than Gold and one day it will be in very short supply BUT... for now I am holding my ZSL postion in the expectation silver will drop. Here is a similar view from someone else: http://www.marketanthropology.com/

http://www.marketanthropology.com/

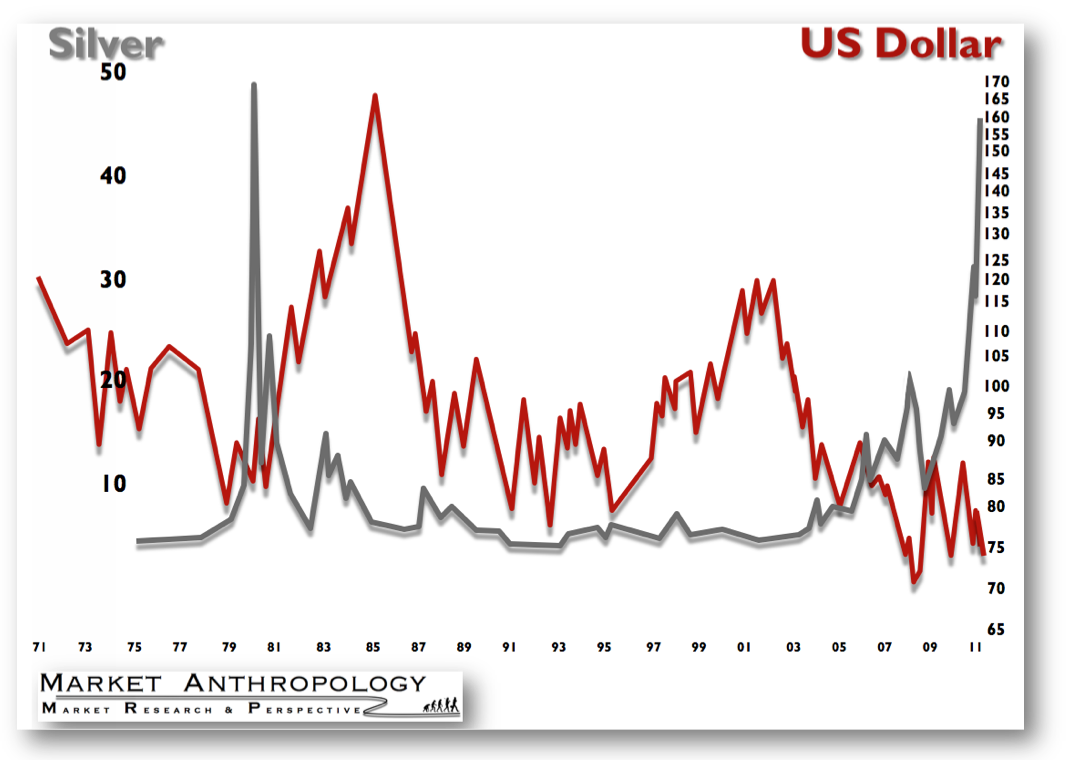

Dollar Holler "I am sitting inside the truck, watching a screen. The truck reels the tool back up out of the hole, slowly - more slowly than if you were reeling it in by hand - and foot by foot, the tool passes through all that dark mystery of time, emitting signals and picking up signals. I watch the tool's response to the formations it passes through on my screen, little green blips of radioactivity, and like an EKG, each blip indicates something... I love to log wells. I've logged a thousand, and I still find myself holding my breath when the tool first starts up out of the hole, when the electronic green lights begin to flicker and race. No one has ever before seen what I am seeing." Rick Bass - Oil Notes Part of the analytical overlay from my previous profession as a geologist is in taking certain data series - stripping away the noise - and extrapolating where things may be and the quality of the information at hand. As a geologist, you are often modeling data from a source that you can not witness in-situ or interact with for more than a few moments. It takes experience, intuition and the ability to render a field that is not readily apparent. "Curiously, however, in geology, when I pour a cup of coffee and sit down and begin to map, I'm not hiding behind anything; there's no pretense, no deceit, just an inquisitive hunger and innocence where I am neither superior nor inferior to the reader, but am the reader. There's truly an amount of trust. The earth lies there, still and obeys certain rules. I have faith that I am not going to let myself believe something that is not true. It is perhaps the purest thing I've ever done. Perhaps that is why geologist become so fervent about a particular prospect. Not holy men, but sill there is that aspect to it - as in athletics, and religions." - Rick Bass I often find that market research today confuses the reader by overindulging the analyst's enthusiasm and concerns towards the subject at hand. When it comes to macro issues, where causation is often a fools game with regards to the daily and weekly market movements, there is an almost unlimited resource of information to pull from in justifying ones expectations. It is the main reason why I find charts so efficient in translating information without the excess baggage often woven into research reports. I find that as long as you have a fundamental understanding of the backdrop (which you get from charts) - focusing your attention on a few pivotal components will yield greater clarity than the nuance that works off of the system itself. Today's almost maniacal obsession with daily and even hourly CDS spreads in Europe comes to mind. We are really just observing the ebbs and flows of energy transmission and momentum in a dynamic system - whether we would call it an open or closed system is open to debate. As traders, do we really need a 2000 word white paper to describe something akin to how a wave translates across a body of water? Certainly you could describe that process in great academic detail if you were arbitraging an esoteric relationship, but for most market participants, a more simple explanation will suffice and likely free you from becoming steeped in confusion and unable to capitalize on developments in the markets in realtime. There is a fine line between perceiving an investor or trader as ignorant - versus someone who has simply discounted information from the big picture. With that said (and certainly hypocritically over-indulged on my end), for those who have been following my notes since the Spring, a great deal of my forecast accuracy and trading acumen have revolved around the notion that the U.S dollar was bottoming and likely to embark upon a significant advance. Having confidence in where I believed the dollar would trade gave me a certain assurance towards shorting silver in the Spring and positioning myself towards an equity market that was going to go through a transitional phase. This in-turn influenced how I approached the markets this summer. ______________________ "For all the dollar bears that are waiting on pins and needles for the bottom to fall out or for America to enter into a hyper-inflationary tailspin, just turn their attention to the historic chart of the American currency, post the Nixon Shock in 71'. Where's the doom and gloom? I see a rather normalized trending currency, reflecting moderate fiat debasement, within a technical framework remarkably similar to late 1980 early 1981. And low and behold, silver has very much been acting within the technical part as it did in 1980. ...This is why I have entered a position that is long the U.S dollar and short silver. It's not a daytrade, it's a thesis position (I can just feel traders cringe)." Time The Great Revelator - 4/23/11 This thesis was based on structural formations in the dollar and the CRB and developments across the Atlantic on the opposite side of the currency pair. ______________________ "Appraising the commodity sector (a component of the everything goes up market), we can see that we have pulled up to both the 61.8% fib retracement level from the 2008 top and what could end up being the right shoulder of a very broad H&S pattern. Considering the commodity trade has been partially a trade against the U.S dollar, and the dollar is about as washed out as it could possibly become from both a technical and sentiment perspective (yes, and even the great currency trader - Matt Drudge, believes the greenback is headed significantly lower) - there remains to be seen what will propel the sector higher at this inflection point." Taking Shelter - 4/28/11 So what comes next? From my perspective, no one should discount how influential and significant a stronger U.S currency is to the financial markets - both here and abroad. Judging by the long-term technical picture, you would have to go back to 1995 and then to 1980 to see a similar set-up. For obvious economic reasons I would argue from a comparative viewpoint that the early 1980's would be a more appropriate precedent of perspective than 1995. Of course these extrapolations are based on the thesis that the U.S currency - as well as the euro - is at a major inflection point. During these contentious times, the financial media will always be louder with their concerns and anxieties, rather than the silver lining imbedded in a development such as this. U.S corporations will certainly have a headwind with their international footprint (some would argue a good thing for domestic investment) and certainly a stronger dollar will make U.S exports more expensive for foreign consumers. Considering that the U.S export story has been one of the only bright spots in an otherwise downtrodden economy - it will be highlighted and pinata-ed by the pundits in the financial media for some time. We are also likely to continue going through a transition where traders do not accept that the stock market can go up at the same time the dollar index appreciates. For many traders today they simply have never witnessed that dynamic for more than a few days to weeks. The dollar goes lower - the stock market goes higher. Eventually the market will transition to a positive correlation with the dollar - the question is just when. This is why to a certain degree I have had more confidence in my expectations for the commodity sector and certain currencies, because I could see those inflection points in the charts. Broadly speaking - the equity markets are currently in no-man's land. I have my suspicions, but the degree of confidence is not the same as in the commodity and currency markets. Irrespective of these concerns, I believe that the trade off will eventually far outweigh the perceived negatives - considering:

- It will come at the expense of high commodity prices - which have been pick-pocketing the U.S consumer and domestic business activity during a very difficult economy.

- It will significantly boost the attractiveness of U.S investments. At a time when analysts and market pundits are wondering where the capital inflows will come from next (especially considering the baby boomer demographic), inflows from foreign investors benefiting from a strengthening currency exchange will be a much welcomed tailwind.

- A stronger currency makes it easier for a nation to borrow and finance its debt. Although that issue has yet to become a real concern, even with the downgrade - in the light of the shenanigans in Congress, we could use all the help we could get.

- The trade deficit will improve (as it did last week). Considering the majority (>50%) of the deficit is comprised of petroleum imports - cheaper energy will benefit the government as well as the consumer.

In summary - the net effect of a strengthening U.S dollar will eventually have real benefits towards the U.S financial markets and our economy. And while it looks pretty darn bleak out there in light of the developments in Europe - the backdrop is always darkest before the dawn. at 11:05 PM

Lots of talk from Europe of the Chinese coming to the rescue. A market that depends on life jackets doesn't work. The dollar was firm but basically unchanged. Silver dropped. I am still holding ZSL and will look for an opportunity to buy back EOU. I am not looking for any other trades until the dust clears a little.

From here on everything is an outright toss up, so I have sold my EUO with a good profit. I have a small position in ZSL . The market is clearly expecting a major ECB stimulus next week. The problem is that it takes time to agree a solution and if one were that easily found they would have already found it. Germany is not going to put up with financing a bunch of lazy non taxpaying economies. So .. anything can happen and it is best to watch from the sidelines. I am staying short silver beacause if everything does lock up, silver will tank. The risk, and this is why it is going up today, is where do you put your money as all the currencies are at risk. The problem to that is if there is no agreement in Europe and its financial markets lock up there will be a lot of people looking for liquidity and that means they will have to sell assets. Silver is a very small market in financial terms and thus very volatile. The only reason I am staying with ZSL is that it has been a good week and I am playing with the market's money.

http://www.scribd.com/doc/64213643/GMA0907-RI-1This is a time to be very careful. I am trading with very close stops on both EUO and ZSL. It is quite possible we could see a global easing and that would force a reversal on both stocks and gold and silver. One has to be prepared to turn on a dime. this is only a market for the fleet of foot.

I have taken some profits in EUO and added to my ZSL position. ZSL is a highly leveraged way of shorting silver.

The President has a way with words and some of the ideas are worth talking about. People like Soros should not be allowed to pay 15% income tax. I would go to jail if I hid my earnings in a Swiss bank account but it is OK for Google, GE and other companies to do so. That is the problem with the Republican Party right now NO MORE TAXES but then we all know some people and companies are getting away with blue murder - Huntsman and Paul may be hard to elect but at least they talk some sense. The President's problem is that he is great with words and short on action - as a former Fed Reserve governor said this evening.. " he could have eased up on drilling restrictions and created a million jobs instantly".

We are back up to our debt ceiling and so we can expect lots of talk from both sides and not much action. That is not good for stocks. It should be good for Gold and Silver and bad for the Dollar but the rest of the world is even worse off so who knows ? I am still looking for a commodity sell off if only because the JPMs of this world need to cover their shorts and will push the market down first. When I can think of a better trade than the ones I have I will let you know. Nothing goes in a straight line .

Why the Dollar Remains the One Essential Currency September 8, 2011 (Mobile version) The only way to value the dollar is in the context of a mercantilist, export-dependent global economy anchored by a sole "importer of last resort," the U.S., which funds these vast imports with its fiat currency, the dollar. Yesterday I explained why a gold-backed currency cannot replace the fiat dollar without fatally disrupting global Capitalism and the political Status Quo everywhere from China to Europe: Why the U.S. Dollar "Works" and Why a Gold-Backed Currency Doesn't (September 7, 2011). Today we look at why the fiat dollar is the one essential currency, and as a result, why it will rise in value in the Eurozone crisis ahead. I know this is heresy and sacrilege to those who believe the dollar is doomed, and soon, but if you're not yet locked into one quasi-religious faith or another just yet, then please follow along as I trace out the dynamics of trade and currency valuation. To understand the essential role of the dollar and how its value is derived via trade flows, let's start with a simplified model of global trade. Country A manufactures surplus goods and generates surplus services. Since its domestic demand is structurally constrained (for example, a mere 35% of China's GDP is domestic demand), the only way Country A can keep its citizens employed and politically pliable is to sell its surplus in other countries. This is the basic mercantilist export model of growth pursued by Germany, Japan, South Korea, China et al.: growth and value are created by generating surplus goods and services, and exporting those to other nations. In sum: Country A has stuff it has to sell to other countries to keep its economy from spiraling into depression. It can demand whatever it wants: gold, moon dust, etc., but it is not in the driver's seat: it has no alternative to dumping its surplus in whatever markets will take it. Managing its exports boils down to getting the best deal possible, but saying "no" is not an option. There is little demand for Country A's currency, as what it is trading isn't currency, it's stuff: it trades its surplus production (stuff) for somebody else's currency. Country B has a something called "the world's reserve currency" which is a fancy name for paper money that is universally recognized as a placeholder of value that can be traded everywhere from Burma (pristine $100 bills preferred) to Bolivia (cocaine-laced $100 bills OK) and accepted without question (even counterfeit bills are OK as long as they're the high-quality North Korean counterfeits). Let's call Country B's currency the doru. Country B has exports, but its demand for imports far exceeds the value of its exports. For all imports over and above the value of its exports, it exchanges its paper money for the imported real goods and services. Country C has no reserve currency and no gold-backed currency. It has paper money which it can print in unlimited quantities. Country C has exports, but its demand for imports far exceeds the value of its exports. For all imports over and above the value of its exports, it exchanges its paper money for the imported real goods and services. Country C has a tricky problem. Since its paper money has no intrinsic value, the only value it can possibly have is scarcity value: the supply must be strictly limited so that exporting nations will accept County C's currency (let's call them quatloos) in exchange for tangible goods like oil and iPads. In effect, Country C is asking exporters to accept a premium on the intrinsically worthless paper, a premium "earned" by scarcity: if there are relatively few quatloos floating around the world, then quatloos may well retain some scarcity value, even though their value based on other factors is basically zero. The best way for Country C to finance its import trade is to exchange its intrinsically worthless quatloos for "the world's reserve currency," the doru, which is accepted everywhere. Some would argue that Country C should buy gold with its quatloos, and that would certainly be an excellent trade: worthless paper for gold. But in terms of trade, shipping gold about is hazardous and costly: every nation engaged in trade needs an electronically traded currency that can be transferred, loaned, borrowed and so on, all in the blink of an eye. Gold is a reliable store of value but it is a cumbersome means of exchange, especially globally. Furthermore, gold's value in currency or other goods has a history of fluctuating wildly. Those managing quatloos could easily get burned, as the trade they're really managing is quatloos to gold to the reserve currency which can actually be traded globally for goods and services. Any such commodity-based transactional chain is rife with risk from geopolitics and speculation. From the managers of the quatloo's perspective, the easiest way to lower risk is to cut out the middle step of buying and selling gold, and just buy the reserve currency (the doru) directly. All this works until Country C succumbs to the temptation to print money to the point it is in surplus rather than scarcity. And what a temptation it is, to "increase our wealth" magically by printing quatloos. But exporters, forced by circumstance to constantly assess the tradable value of all currencies they trade goods for, will quickly detect that the scarcity value of the quatloo--it's only real value--has rapidly declined. The cost of imports priced in quatloos in Country C shoots up as quatloos lose scarcity value, and the residents of Country C find they can no longer afford to buy imports. The sales of imports collapses down to match Country C's exports. These are the key dynamics of trade and currency valuation. Now let's consider Country B, owner of "the world's reserve currency," the doru. Superficially, it might seem that the only value in dorus is also their scarcity value, and since Country B prints/creates large quantities of dorus every year, many observers make the understandable mistake of claiming the value of the doru should be zero, since it is has little to no scarcity value. But the value of "the world's reserve currency" is not simply a matter of scarcity, as it is for other lesser fiat (paper) currencies. One factor is the nature of scarcity is different for the doru and the quatloo: the quatloo has only one use in terms of global trade: the imports and exports of Country C. Since Country C's GDP is a thin sliver of global GDP, then demand for quatloos is limited to importers and tourists. Compare that to "the world's reserve currency," which is in constant demand as a means of exchange in the entire $60 trillion global economy. "The world's reserve currency" (in our example, the doru) has another unique feature: everybody eventually needs to exchange quatloos and all other currencies for doru, because that is the only universally accepted means of global exchange. Sure, Country C and its cronies can set up an exchange which only accepts gold and quatloos, but as soon as they need wheat, electronics, and everything else the cronies don't manufacture or harvest, then they will need to exchange the gold or quatloos for "the world's reserve currency." As a result, the demand for doru ("the world's reserve currency") is stupendous and constant. Since currency is a commodity, albeit one with unique features, its ultimate value as a means of exchange is set by supply and demand. In other words, scarcity is not the only source of value: demand is the key driver of value of any commodity, good or service. Let's say that Country B's economy is about 25% of global GDP. (In other words, like the U.S.) Let's further assume that Country B prints/creates about 10% of its GDP every year in paper doru. Now if Country C printed 10% of its GDP every year in newly issued quatloos, the supply of quatloos would quickly overwhelm demand for quatloos, and the value of quatloos globally would crash. Country B doesn't have that problem, because printing 10% of its GDP is a mere 2.5% of global GDP. Globally, the value of currencies exchanged daily exceeds 10% of Country B's GDP and more or less matches the total value of doru in global trade. In other words, the demand for exchangable, tradable currency--"the world's reserve currency"-- far exceeds the supply of doru. Printing doru, even in quantity, is like adding a glass of water to a bathtub: the supply increase is not even close to the daily demand. How did Country B get the "the world's reserve currency" instead of Country C? Most importantly, there has to be enough of the currency to grease the tremendous flows of goods, services, loans and hedges globally: the tiny quantity of quatloos is completely inadequate to the task. Second, the "the world's reserve currency" must be relatively immune to increases in supply, i.e. money printing. For example, if global GDP is $60 trillion, and daily foreign-exchange trading is $2 trillion, then exactly how much impact can printing $1 trillion of "the world's reserve currency" generate? The answer globally is very little. The third factor is one which few commentators recognize, sometimes called "the hidden export:" global security. All financial transactions involve trust, some more than others. In terms of currency, the primary trust being offered and accepted is that the mechanics of the currency are transparent and thus so are the risks. The secondary trust is that the value of the currency will remain stable over the short term, which is long enough for the vast majority of trading. A third trust is in the stability of the issuing nation. Once again, transparency is key: if that nation's problems are well-known and transparent, then the risks of that currency can be easily and accurately assessed. If its institutions are robust and its trade flows gigantic, then people recognize it's a safer bet to hold dorus than quatloos. The key mechanism for creating surplus value in advanced Capitalism is trade, and the key mechanism for enabling that trade is a "reserve currency" of sufficient quantity and stability. The Chinese renminbi is a proxy for the U.S. dollar, the euro is unraveling, and the yen is not expansive enough to fund global trade and currency flows. Envy is a key human trait, and the envy of all those who don't hold/print "the world's reserve currency" is understandable. But you can't create "the world's reserve currency" like some other paper money, as paper money only has two sources of value: demand and trust. As Jesse of the always-valuable Jesse's Cafe Americain recently wrote (and I paraphrase), people often offer reasons why certain things that have happened could not happen. Conversely, they also often offer reasons why things that can't happen should happen. At some point the trade imbalance of $600 billion a year between the mercantilist nations and the U.S. will go away, as will the notion that printing paper money is creating wealth, and debts that are unpayable will magically be paid instead of being liquidated or repudiated. The point here is that the Status Quo of all the major trading nations is committed to conserving the present system of fraying imbalances, as their own wealth and power flow from this shaky, unsustainable structure.

← DAX coming off Inflation vs Deflation? → If you’re looking for bubbles, don’t look at gold coins-Dr Constantin Gurdgiev Posted on 8 September, 2011, 03:07, UTC+1 by the trader From Gold Core,Dr. Dr Constantin Gurdgiev, Head of Research with St Columbanus AG, member of the investment committee of GoldCore and the adjunct lecturer in finance in Trinity College, Dublin,Of all asset classes in today’s markets, gold is unique. And for a number of reasons.* Firstly it acts as a long-term hedge and a short-term flight to safety instrument against virtually all other asset classes.** Secondly, it supports a wide range of instruments, including physical delivery (bullions, coins and jewellery), gold-linked legal tender, gold-based savings accounts, plain vanilla and synthetic ETFs, derivatives and producers-linked equities and funds. All of these are subject to diverse behavioural drivers of demand. Thirdly, gold is psychologically and analytically divisive, with media coverage oscillating between those who see gold as either a long-term risk management tool, or a speculative “bubble”. In the latter context, it is interesting to look closer at the less-publicized instrument — gold coins, traditionally held by retail investors as portable units to store wealth. Due to this, plus demand from collectors, gold coins are less liquid and represent more of a pure ‘store of value’ than a speculative instrument. Classical bubbles arise when speculative motives (bets on continued accelerating price appreciation) exceed fundamentals-driven motives for holding gold. In later stages of the “bubble”, we should, therefore, expect demand for gold coins to fall compared to the demand for financially instrumented gold. The U.S. Mint data on sales of gold coins suggests that we are not in the last days of the “bubble”. But there are warning signs to watch into the future. August sales by the U.S. Mint were up a whooping 170 per cent year on year in terms of total number of coins sold, while the weight of coins sold is up 194 per cent. On the surface, this gives some support to the theory of gold becoming overbought by retail investors. However, monthly comparatives reflect a huge degree of volatility in U.S. Mint sales and August results comfortably fit within statistical normals for the crisis period since January, 2008. August results also fall within the historical mean (1987 through Monday). At 112,000 oz of gold coins sold, August, 2011 is only the 19th busiest month in sales since January, 2008. Since 1988 there were 87 months in which average gold content per coin sold by the U.S. Mint exceeded the August, 2011 average and on 38 occasions, volumes of gold sold exceeded last month’s. In other words, current gold coinage sales do not represent a dramatic uptick in demand. The data also shows that physical demand for coins is largely independent of the spot price of gold. Historically, since 1986, average 12-months rolling correlation between the spot price of gold and the volumes of gold sold in US Mint coins is negative at -0.09. Since January, 2008, the average correlation is -0.2. And over the last 3 years, the trend direction of gold spot price (up) and the volumes of gold sold in coinage (down) have actually diverged. The latter is, of course, concerning and will require closer tracking in months to come.

The chart above also highlights the fact that the current trend levels of U.S. Mint sales are significantly elevated on previous periods, with the exception of 1986-1987 and 1998-1999 demand spikes. Since the global economic crisis began, annual coinage sales rose sevenfold, from just under 200,000 oz in 2007 to 1,435,000 oz in 2009, before falling back to 1,220,500 oz in 2010. Using data through August, I expect 2011 sales to remain at around 1,275,000 oz.

|

RSS Feed

RSS Feed

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}